{kind=link}

This section is Presented

This section was created by the editors. The client was not given the opportunity to restrict the content or to check it before publication.

from RBC Mortgages

Breadcrumb Trail Links

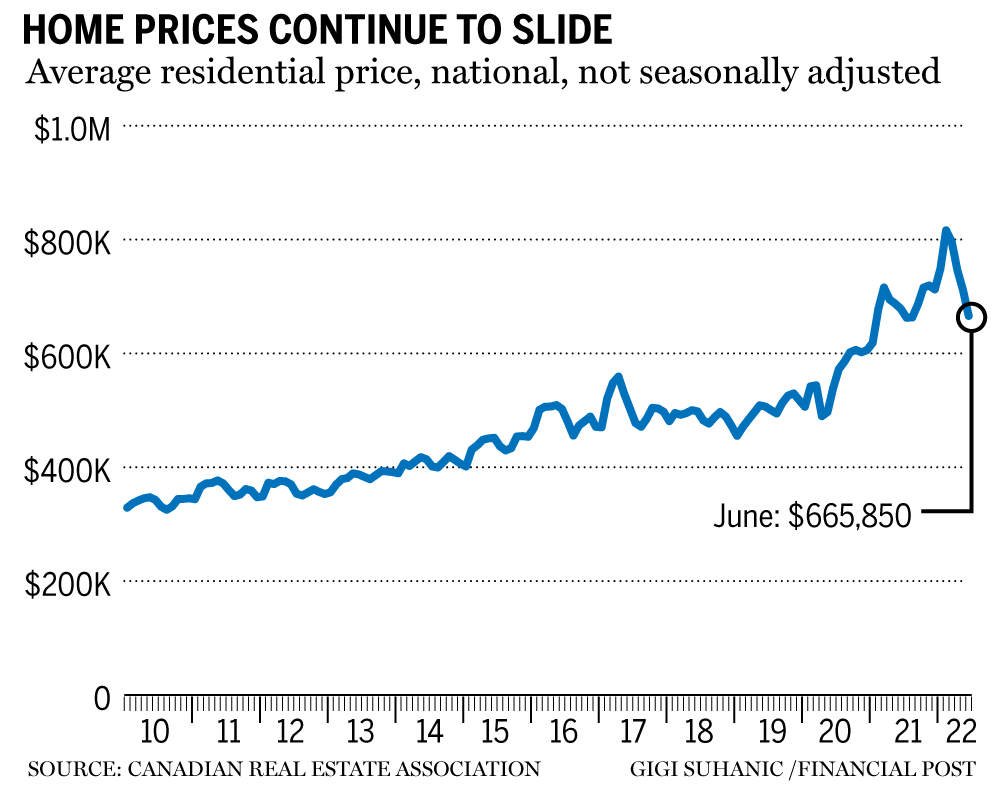

The median price in June was $665,850, down 2 percent year-on-year and 6 percent down from May

A for sale sign on a home outside of Ottawa. Photo by Ashley Fraser/Postmedia

A for sale sign on a home outside of Ottawa. Photo by Ashley Fraser/Postmedia

content of the article

Toronto real estate agent Harry Sarvaiya was ready for higher interest rates, but not like this.

advertising 2

This ad has not yet loaded, but your article continues below.

content of the article

“I think the intent came as a shock,” Sarvaiya said a few days after the Bank of Canada raised the benchmark a full percentage point, the largest increase since 1998. “In real estate, people didn’t expect it.”

Home construction is probably the industry most sensitive to interest rates. This is helpful when the economy is in trouble. The central bank can quickly stoke demand by lowering interest rates, knowing that Canadians will buy homes — and then renovate them and fill them with expensive items like appliances and furniture. Service providers such as banks, brokers, contractors and movers all benefit.

content of the article

If prices continue to rise, the broader economy will benefit as households feel richer, which economists call the “wealth effect”.

advertising 3

This ad has not yet loaded, but your article continues below.

content of the article

Canada’s economic growth over the past decade has depended heavily on such wealth effects. But the central bank’s job is not to attack the housing market; Their job is to control inflation, which accelerated to nearly 8 percent in May.

Bank of Canada Governor Tiff Macklem has now increased borrowing costs more in the past four months than his predecessors did in the decade between the end of the Great Recession and the onset of the pandemic. The impact on the housing market has been just as immediate as it was when borrowing costs were reduced to near zero, but not nearly as pleasant for the real estate industry and aspiring buyers and sellers.

“Everything has happened to us in the past few weeks,” said Joe Baglieri, a broker at Re/Max Realtron Property Shop in Markham, Ontario. “We had deals that fell through, we had renegotiations.”

advertising 4

This ad has not yet loaded, but your article continues below.

content of the article

Baglieri said real estate is more of a long-term game and anyone involved in it should expect cooler periods. The problem is that borrowing costs have been so low for so long that many households have forgotten what it’s like when interest rates bite. Geoff Morgan, a Toronto-based brand marketer, said his bank raised its adjustable-rate mortgage rate within hours of the Bank of Canada’s shock policy announcement on July 13, while its adjustable-rate savings account showed little movement.

“I asked my bank for an explanation,” Morgan said. “They tell me they offer competitive prices.”

The impact goes beyond the burden on current homeowners. Home sales and prices continue to slide across the country as rising mortgage costs spill over into the market and sideline more homebuyers. Sarvaiya said he lost a sale of a $400,000 Toronto condo because the buyer didn’t qualify for the mortgage.

advertising 5

This ad has not yet loaded, but your article continues below.

content of the article

“He had the 20 percent deposit, but after that, the ratios are,” Sarvaiya said. “He has to qualify for Prime plus Two, which he would easily have two months later and now it’s difficult to qualify.”

The Canadian Real Estate Association reported July 15 that the nationwide actual, non-seasonally adjusted average price was $665,850 in June, down nearly 2 percent year-on-year and down 6 percent from May.

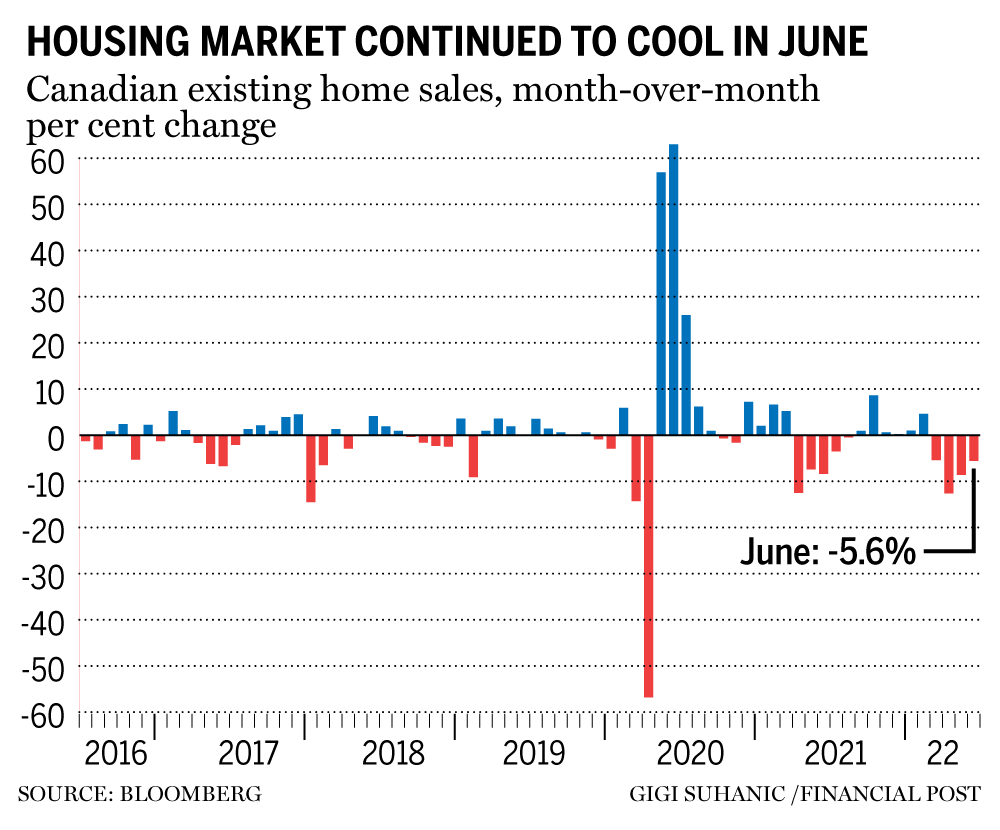

The number of home moves fell 5.6 percent month-on-month in June, down about 24 percent from the June 2021 record. The federation noted that the declines were not as large as the declines seen in April and May.

“Selling activity continues to slow amid rising interest rates and uncertainty,” CREA chair Jill Oudil said in a press release accompanying the data. “The cost of borrowing has overtaken supply as the dominant factor affecting housing markets right now, but the supply problem has not gone away.”

advertising 6

This ad has not yet loaded, but your article continues below.

content of the article

Lauren Haw, chief executive officer of Zoocasa Realty Inc., told the Financial Post’s Larysa Harapyn in a July 12 interview that more and more Canadians are holding back their purchases and waiting to see what the Bank of Canada would do next.

“As people are saying, just let the dust settle before you make that big decision,” Haw said. “So that means there’s a lot of contortions and people are just sitting on the edge.”

Haw added that prospective homebuyers are waiting for signs that prices have bottomed before getting back on the market.

The Bank of Canada noted in its latest quarterly report that a “sharp slowdown” in housing construction was “underway.” Robert Kavcic, an economist at Bank of Montreal, called the latest data the “early days of correction” in a note to clients.

advertising 7

This ad has not yet loaded, but your article continues below.

content of the article

“Sales have now fallen back into pre-COVID levels and below the 10-year moving average for the first time since the pandemic began,” Kavcic wrote in a note to customers. “The period of extreme excess demand is essentially over and we are headed for a very weak year in terms of resale volumes and prices.”

-

What the Bank of Canada’s full percentage point hike means for the housing market and your mortgage

-

‘I’m desperate’: Jumbo rate hike adds more financial pain to some Canadians

-

Royal LePage lowers home price outlook ‘significantly’ on aggressive Bank of Canada rate hikes

-

Canadians flocked to adjustable-rate mortgages ahead of Bank of Canada rate hikes, CMHC says

Some are already warning that Canada is headed for a real estate bankruptcy. At the same time, some of these people have been saying this for more than a decade. Christopher Alexander, President of Re/Max Canada, argued that the exuberant average price growth during the pandemic has not been sustainable and that higher interest rates would make the market healthier.

advertising 8

This ad has not yet loaded, but your article continues below.

content of the article

“This is good news for buyers and sellers who need to navigate the market, and ultimately good news for the real estate professionals who serve them,” Alexander said. “A healthy market growing in the mid to high single digits will allow more Canadians to enter the market. The real challenge for consumers and the real estate industry will be the shortage of supply.”

Kelsey Smith, who wants to buy her first home in Calgary, said finding a home and buying a mortgage has become much more difficult. The recent MBA grad said she plans not to lock herself into a five-year fixed-rate mortgage, although she doesn’t like the idea of ”roller coaster rides” with variable rates.

“I’ve decided to lower my price range by $50,000 because of current interest rates,” she said. “On the mortgage front, I had to consider changing the payback period from 25 years to 15 years – I was actively trying to provide MacGyver with a path to a better business myself. It kind of sucked.”

Back in Toronto, Sarvaiya prepared for a new reality. The “madness” of bidding $100,000 too much is over, he said. “Right now all these houses are for sale and no one is buying even if they’ve lowered the price because the buyer lost confidence thinking there was going to be a downward spiral,” he said.

Additional reporting from Marisa Coulton, Denise Paglinawan and Meghan Potkins.

• Email: [email protected] | Twitter: StephHughes95

Share this article on your social network

advertisement

This ad has not yet loaded, but your article continues below.

![]()

Financial post top stories

By clicking the subscribe button, you agree to receive the above newsletter from Postmedia Network Inc. You can unsubscribe at any time by clicking the unsubscribe link at the bottom of our emails. Postmedia Network Inc | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for registering!

Comments

Postmedia strives to maintain a lively but civilized discussion forum and encourages all readers to share their opinions on our articles. Comments may take up to an hour to be moderated before they appear on the site. We ask that you keep your comments relevant and respectful. We’ve turned on email notifications – you’ll now receive an email when you get a reply to your comment, there’s an update on a comment thread you follow, or when a user you follow comments follows. For more information and details on how to customize your email settings, see our Community Guidelines.